One simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

The most you can lose on any stock (assuming you don’t use leverage) is 100% of your money. But in contrast you can make much more than 100% if the company does well. For instance the Ulta Beauty, Inc. share price is 191% higher than it was three years ago. Most would be happy with that. It’s also good to see the share price up 13% over the last quarter. But this could be related to the strong market, which is up 6.2% in the last three months.

So let’s investigate and see if the longer term performance of the company has been in line with the underlying business’ progress.

During three years of share price growth, Ulta Beauty achieved compound earnings per share growth of 27% per year. This EPS growth is lower than the 43% average annual increase in the share price. So it’s fair to assume the market has a higher opinion of the business than it did three years ago. That’s not necessarily surprising considering the three-year track record of earnings growth.

Our analysis is essentially based on how sell-side analysts covering the stock are revising their earnings estimates to take the latest business trends into account. When earnings estimates for a company go up, the fair value for its stock goes up as well. And when a stock’s fair value is higher than its current market price, investors tend to buy the stock, resulting in its price moving upward. Because of this, empirical studies indicate a strong correlation between trends in earnings estimate revisions and short-term stock price movements.

Ulta is expected to post earnings of $6.75 per share for the current quarter, representing a year-over-year change of +7.1%. Over the last 30 days, the Zacks Consensus Estimate has changed +4.4%.

Marriott International, Inc. MAR is scheduled to release fourth-quarter 2022 results on Feb 14, 2023, before the opening bell. In the previous quarter, the company’s earnings matched the Zacks Consensus Estimate of $1.69.

The Trend in Estimate Revision

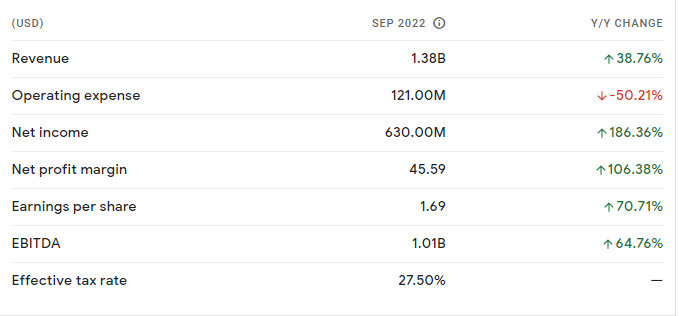

The Zacks Consensus Estimate for the fourth-quarter bottom line is pegged at $1.84 per share, indicating growth of 41.5% from $1.30 reported in the year-ago quarter.

For revenues, the consensus mark is pegged at $5,612 million, suggesting growth of 26.2% from the prior-year quarter’s reported figure.

Key Factors to Note

Marriot’s fourth-quarter performance is likely to have benefited from robust leisure demand and business and cross-border travel improvements. During the previous-quarter earnings call, the company stated that cross-border guests accounted for 15% of global room nights, up from 12% reported in the first quarter of 2022. Also, it reported a rise in last-minute booking trends, thereby leading to a meaningful compression in pricing power and boosting group ADR for new bookings.

With global trends improving, the recovery momentum is likely to have continued in the fourth quarter. Attributes such as pent-up demand for all types of travel, the shift of spending toward experiences versus goods, sustained high levels of employment and resilient travel spending are likely to have boosted the company’s performance in the to-be-reported quarter.

Increased focus on the Marriott Bonvoy loyalty program bodes well for the company. With nearly 173 million members globally, the company’s loyalty program Marriott Bonvoy is supporting its marketing strategies. The company engages its customers with promotional offers such as grocery and retail spending accelerators on its co-branded credit cards. During the third quarter of 2022, the program reported solid penetration levels of 60% in the United States and Canada and 53% globally. Also, the company reported increased sign-ups following the addition of new benefits to its U.S. cards. Given the meaningful pickup in demand coupled with solid customer acceptance for credit card programs, the momentum is likely to have continued in the fourth quarter.

The Zacks Consensus Estimate for fourth-quarter revenues at base management and franchise fees is pegged at $282 million and $674 million, indicating year-over-year growth of 30% and 29.6%, respectively.

However, coronavirus-induced travel restrictions (in China) and supply chain disruptions are likely to have affected the company’s operations in the third quarter. Although revenue per available room (RevPAR) is likely to have increased sequentially in Greater China and Asia Pacific (excluding China), it is expected to have remained below pre-pandemic levels.

What the Zacks Model Unveils

Our proven model predicts an earnings beat for Marriott this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat.

Earnings ESP: Marriott has an Earnings ESP of +1.63%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Kgoo Episode 22

Kgoo Episode 22 Kgoo Episode 21

Kgoo Episode 21 Kgoo Episode 38

Kgoo Episode 38 Kgoo Episode 48

Kgoo Episode 48 Kgoo Episode 14

Kgoo Episode 14 Kgoo Episode 10

Kgoo Episode 10 KGOO Episode 5

KGOO Episode 5