The argument over which type of account to use typically revolves around how much money you make. Early-career, low-income workers are better off in a Roth, the thinking goes, because they’d save money by paying taxes when they’re in a low bracket instead of waiting until they’re bringing in more in retirement. High earners, meanwhile, are generally steered toward traditional accounts and their upfront tax break.

The key difference between traditional and Roth retirement accounts is when you pay taxes. Here are some additional insights:

Traditional Accounts

Pre-Tax Contributions: Contributions are made with pre-tax dollars, reducing your taxable income for the year you contribute.

Tax-Deferred Growth: Your investments grow tax-deferred, meaning you don’t pay taxes on gains until you withdraw the money.

Taxable Withdrawals: Withdrawals in retirement are taxed as ordinary income.

Roth Accounts

After-Tax Contributions: Contributions are made with after-tax dollars, so you pay taxes upfront.

Tax-Free Growth: Your investments grow tax-free, and qualified withdrawals in retirement are also tax-free.

Flexibility: You can withdraw your contributions (but not the earnings) at any time without penalties.

Considerations

Income Level: Early-career, low-income workers might benefit more from Roth accounts, as they pay taxes at a lower rate now rather than potentially higher rates in retirement.

Tax Rates: High earners might prefer traditional accounts for the immediate tax break, especially if they expect to be in a lower tax bracket in retirement.

Tax Diversification: Having a mix of both account types can provide flexibility and tax advantages in retirement.

It’s always a good idea to consult with a financial advisor to determine the best strategy for your specific situation.

Achieving financial success often requires more than just the basic advice of saving and investing. We’ve asked ChatGPT for some ideas outside of the box to boost savings and wealth. Here are ten unusual but effective strategies that can propel you towards financial prosperity:

Managing your personal finances can be tricky if you don’t have the strategies and guidance you need. Organization, research, planning and funding are all necessary to achieve your financial goals. On Google.com, you can learn about different investment strategies and how to make your money work for you.

If you’re interested in stocks, CD accounts, real estate, investment funds, collecting valuables or any other investment, ChatGPT has the information you need. You’ll find articles that explain the difference between different types of investments, breakdowns of investment methods, advice on what types of investments are most likely to be successful and even entertaining news stories about investing.

So whether you’re planning on making a big investment by purchasing property or you’re preparing to make a smaller investment, ChatGPT can help.

1. Practice Frugality in Unconventional Ways

Challenge conventional spending habits. For instance, embrace a minimalist wardrobe or use public transport instead of owning a car. These unconventional choices can lead to significant long-term savings.

2. Invest in Learning Over Entertainment

Redirect funds typically spent on entertainment towards educational resources or courses. This investment in knowledge can pay off exponentially in terms of career advancement and income opportunities.

3. Automate Savings into an ‘Inconvenience’ Account

Set up an automatic transfer to a savings account at a different bank, ideally one that’s a bit inconvenient to access. The extra effort needed to withdraw funds can deter impulsive spending. And DO NOT take money out of the random business ATM machine. Those habits do not bring on the mindset of achieving financial success.

4. Turn Your Hobby into a Side Hustle

Monetize your passion or hobby. Whether it’s crafting, coding, or cooking, find a way to earn from what you love doing in your spare time. The most profitable people are profiting on the thing they love the most. If you love your product, so will the customer.

5. Embrace Bartering and Trading

Instead of purchasing new items, consider bartering services or goods with friends, family, or local communities. This can be a creative way to get what you need without spending money.

6. ‘Freeze’ Your Credit Card for Emergencies

Literally freeze your credit card in a block of ice. This makes it available for genuine emergencies only and prevents impulsive use.

7. Practice the 30-Day Rule

Delay non-essential purchases for 30 days. Often, the urge to buy dissipates over time, saving you from unnecessary spending. Overtime you realize a lot of the extras you were spending on didn’t have much of an impact on your overall happiness, and will become most likely happier with the amount of discipline and savings you’ve achieved.

8. Rent Out Unused Space or Items

If you have an extra room, parking space, or even seldom-used tools, consider renting them out. This can be a steady source of passive income.

9. Invest in Sustainable Living

Incorporate sustainable practices like growing your own vegetables or installing solar panels. These actions reduce living costs and benefit the environment.

10. Use ‘Gamification’ for Saving

Turn saving money into a game. Set challenges, such as ‘no spend’ days or competing with a friend to save a certain amount each month. This makes the process of saving more engaging and motivating.

Financial success is often a blend of conventional wisdom and creative strategies. By adopting these unusual yet practical methods, you can develop a stronger, more resilient approach to managing and growing your wealth.

Some of Wall Street’s major stock indexes remain below their all-time highs, which means bargains can still be found.

Most online brokerages have done away with commission fees and minimum-deposit requirements, making it easier than ever for retail investors to put their money to work.

Three time-tested companies possess the necessary growth catalysts to make patient investors notably richer.

You don’t need a mountain of cash to build wealth on Wall Street.

Investing on Wall Street can sometimes be a roller coaster of emotions. The COVID-19 crash in February-March 2020 was the quickest bear market decline in history. Meanwhile, the rallies growth-stock investors have enjoyed in 2021 and 2023 have been jaw-dropping.

Despite these notable gains, some of Wall Street’s most followed indexes (e.g., the Nasdaq Composite) remain below their all-time closing highs. Put another way, high-quality stocks can still be purchased at a discount if you’re willing to put in the work and look for bargains.

What’s particularly noteworthy about putting your money to work on Wall Street is that prior barriers to investment have been all but torn down. Most online brokerages have completely done away with minimum-deposit requirements and commission fees for common stock trades executed on major U.S. exchanges. In other words, any amount of money — even $500 — can be the ideal amount to put to work.

If you have $500 that’s ready to invest, and this isn’t cash that’ll be needed to pay bills or cover an emergency, the following three stocks stand out as no-brainer buys right now.

Visa

The first genius stock you can confidently add to your portfolio with $500 is world-leading payment processor Visa(V). Even though Visa shares are near an all-time high, the company sports a laundry list of competitive advantages that should continue to lift its valuation for years, if not decades, to come.

The interesting thing about Visa is that its biggest headwind is also its greatest opportunity. Like most financial stocks, Visa is cyclical. This is to say that its operating performance tends to ebb and flow with the health of the U.S. and global economy. If a recession takes place, consumer and enterprise spending would be expected to decline, leading to weaker fee collection for Visa.

However, the “ebbs” don’t last nearly as long as the “flows.” Only three of the 12 U.S. recessions since World War II have lasted at least one year. By comparison, most periods of expansion last multiple years, with two expansions lasting a full decade. Visa is perfectly positioned to take advantage of these extended periods of growth.

To add to the above point, Visa’s growth runway during these long-winded expansions is enormous. As of 2021, it held a nearly 53% share of credit card network-purchase volume in the United States. Meanwhile, faster-growing emerging-market regions, including the Middle East, Africa, and Southeastern Asia, remain largely underbanked and therefore ripe for disruption by financial-services providers like Visa.

Something else that’s been critical to Visa’s long-term success is its avoidance of lending. Visa is a well-known and trusted brand, and it would likely succeed as a lender. But doing so would also expose the company to credit delinquencies and loan losses during inevitable economic slowdowns. Completely avoiding the lending arena means not having to set aside capital for potential losses. It’s one of the key reasons Visa bounces back from recessions so quickly.

Lastly, Visa is a cash cow with a profit margin north of 50%. Although its forward price-to-earnings (P/E) ratio of 23 is higher than the benchmark S&P 500, Visa’s expected annualized earnings-growth rate of 14% over the next five years makes its stock a bargain.

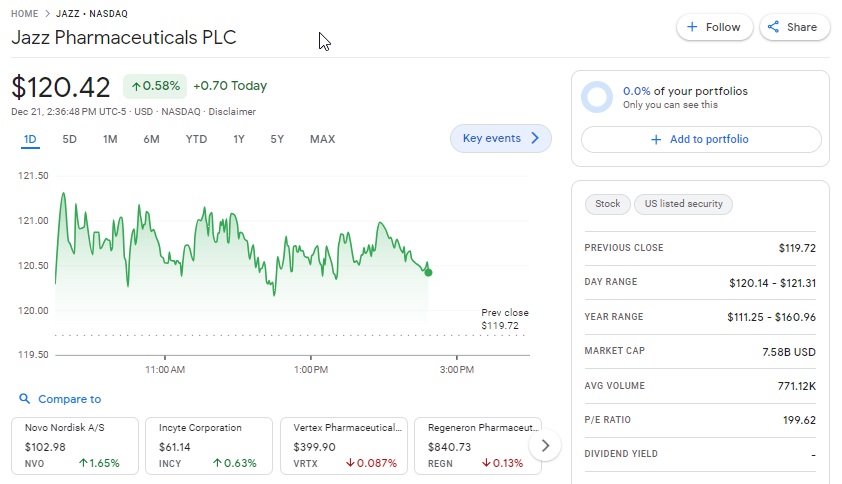

Jazz Pharmaceuticals

A second no-brainer stock with an exceptionally favorable risk-versus-reward profile for patient investors is specialty healthcare companyJazz Pharmaceuticals(JAZZ).

The enemy of pretty much every drug developer is time. Novel therapies have finite periods of sales exclusivity. Once those periods of exclusivity end, it’s not uncommon for generic drugs and/or biosimilar competition to enter the space and either siphon away sales or reduce the average selling price for a product. Jazz generates about half of its revenue from its oxybate franchise (Xywav and Xyrem), which help patients with various sleep disorders. A high concentration of sales in one franchise/area of focus can be worrisome.

However, Jazz Pharmaceuticals has its bases covered. The company developed a next-generation version of its narcolepsy blockbuster Xyrem. This new version, known as Xywav, contains 92% less sodium than its predecessor. Not only does this make Jazz’s drug safer to take for patients with higher cardiovascular risk factors, but it’ll help preserve the company’s cash flow and sales exclusivity for many years to come.

Jazz’s oncology portfolio is also gaining momentum. Cancer-drug sales look to be on track to reach $1 billion in 2023, with acute lymphoblastic leukemia therapy Rylaze doing a lot of the heavy lifting with sales up 46% year to date to $292.5 million.

Cannabidiol-based drug Epidiolex is holding its own as well. Since Jazz acquired GW Pharmaceuticals in May 2021 to get its hands on Epidiolex, sales have continued to grow. Additional worldwide approvals, along with label-expansion opportunities, have the ability to eventually push Epidiolex’s annual sales past $1 billion.

Don’t overlook Jazz’s pipeline, either. The company anticipates as many as five late-stage trial readouts before the end of 2024, with many of these advanced studies focused on experimental cancer drugs.

The third no-brainer stock to buy with $500 right now, conglomerate Berkshire Hathaway(BRK.A) (BRK.B), may not be a household name, but its billionaire CEO, Warren Buffett, certainly is. Take note, I’m specifically talking about Berkshire’s Class B shares (BRK.B), since a single Class A share will set an investor back more than $544,000!

Since the Oracle of Omaha became CEO in 1965, he’s overseen a 19.8% annualized return in his company’s Class A shares (BRK.A). The Class B shares weren’t issued until 1996, which is why I’m referring to returns of the Class A shares in this instance. Even if Berkshire fails to return close to 20% on an annualized basis moving forward, Buffett and his team have clearly demonstrated their ability to outpace the broader market over long periods.

One of the factors that makes Berkshire Hathaway such a special investment, other than Warren Buffett, is its focus on cyclical businesses.

Buffett and the late Charlie Munger, who served as Berkshire’s vice chairman for 45 years, realized a long time ago that betting on the U.S. economy to grow over time is a smart idea. Instead of trying to guess when recessions would occur, Buffett and Munger packed Berkshire’s investment portfolio and owned assets with time-tested, profitable, cyclical businesses. Thanks to extended periods of economic expansion, these long-term holdings have delivered big gains for Berkshire and its shareholders.

Another unsung hero for Berkshire Hathaway is the myriad of dividend stocks that sit in its investment portfolio. Over the course of the next year, Buffett and his investing aides will oversee the collection of around $6 billion in dividend income. On top of being recurringly profitable, dividend stocks have historically run circles around publicly traded companies that don’t offer a payout.

Furthermore, the culture that Charlie Munger instilled at Berkshire Hathaway is going to live on for decades to come. While every investor would love to see Warren Buffett live to be 120, the truth is that he and Munger built Berkshire Hathaway to succeed long after they’re gone. If the American economy is growing over time, there’s a good chance Berkshire’s wholly owned subsidiaries, which include insurer GEICO and railroad BNSF, as well as the company’s $374 billion investment portfolio, are going to benefit.

Should you invest $1,000 in Visa right now?

Before you buy stock in Visa, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Visa wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $294,765!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has nearly quadrupled the return of S&P 500 since 2002*.