New attractions and interest into major construction endeavors has driven the expansion and remodel of the world’s major cities, meeting the needs and expectations of group activities to be able to take place wherever scheduled. The planning and redistribution of funds into projects such as these across the board comes with its challenges, keeping the crews alert throughout the lifecycle of such major projects. Management, entertainment, amenities, and supplies play a key role in running these businesses within most of our magnificent locations, moving employees from one location to another, keeping a steady flow and expectations to our guests.

Our utilities facilities and subsidiary corporations are working continuously around the clock, making sure our main necessities and supplies are met from fuel gasoline, hydrate fuel, expansion and

maintenance of roads, water supplies and food delivery trucking coast to coast. Our power generation systems and auxiliaries wind mills power supplies can seen and spotted along our highways which

cannot be taken for granted. We are blessed to have both rural and urban amenities to balance our ecosystems, keeping us in check and competitive with our global competitors.

Partnering with our global competitors have continuously strive to improve our standard of living and making major impacts to the tourism world across the board. Today, International markets and living estates are present in major cities and local rural areas, depending on the needs of such diversity. Education facilities comes with all necessary accommodation to meet our expectations. Good listening and learning from our educators, has driven us to a new level and will continue to challenge us from generations to generations to come.

The booming of information technologies continue to facilitate the delivery of data information to all comprising of every information you may come across, keeping majority of the mainstream in sync. Maintaining a steady flow while innovating our current systems with creativity and modifications by our technology and manufacturing corporations, eradicating most of the defects and bugs identified through R&D facilities. Most of these topics mentioned on this article can be viewed and discussed on GOOGLE. Feel free to leave a comment.

Involving business when developing suburbs and inner cities, it is necessary and helpful to bring different construction business together to work and partner as teams. These construction contractors / business intend becomes affiliated to related defined projects as such while development becomes identify and progresses throughout different locations. The bonding formed during such constructions go a long way and should be nurtured by maintaining the same group of construction corporations while introducing new once into the market.

Capitalism on performance and profitability has driven business in to a new height, keeping their goals in positive momentum while addressing remodeling and maintaining their structures. The infrastructure units necessary for such developments may be put in place by one or many construction business depending on the magnitude and location of the projects.

Feasibility studies of similar projects are mostly used in deriving the current expense of newly defined projects to come up with a ballpark estimate before involving regular investors into the business deal. Its’ always nice to have projected deals lined up although the constant continuity set forth for these corporations to advertise their projects are necessary to maintain their customers and clients, to strive in meeting the companies’ bottom line giving investors a reason to invest in their markets and corporations.

SVEN Corporation is a typical corporation doing business in many sectors to meet up with the demand of both population and location driven business both locally and globally depending on the demands. I will advice investors to depend and invest on corporations like this. Good timing to hold and buy.

Lately we have come to believe soda is good for the body depending on how it is consumed and the ingredients (nutrition facts) use for producing such mixture. Orange sodas are usually health for our brains and gives a libido sensation to rejuvenate our memories when combine with water.

A combination of plain sodas such as seven-up, Schweppes ginger ales, Canada dry and tonic are perfect to mix up with colored sodas, adding 1/4 amount of water of the total mixture. Fruit drinks may be added into the mixture to produce a delicious quash combination. Its’ lite and good for entertaining any group during or after hours on working days as well as weekends.

Others may debate if cans are preferable than bottled products which may all depend on what exactly are the attributes to the discussions before identifying why it may not be necessary to consume products from either group of packaging. Others may prefer plastic containers as compared to both cans nor bottles.

It is crucial for the beverage companies to identify if any sediments from these packages may be in some of their products within a certain number of period if not consumed. Although such doubt has been eliminated by improving on packaging, it’s always nice to keep track of such maladies. In such circumstances, research and development may be initiatives to get back to the drawing board to determine and resolve such issues.

It could occur that these underlining issues are due to compression and/or expansion index used during the formation of these packages or the swirl effects generated on such liquids before sealed. So far they have not been any major maladies due to sodas nor combination of sodas to produce quashes.

Try adding water and find out from yourself what is preferable.

One simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

The most you can lose on any stock (assuming you don’t use leverage) is 100% of your money. But in contrast you can make much more than 100% if the company does well. For instance the Ulta Beauty, Inc. share price is 191% higher than it was three years ago. Most would be happy with that. It’s also good to see the share price up 13% over the last quarter. But this could be related to the strong market, which is up 6.2% in the last three months.

So let’s investigate and see if the longer term performance of the company has been in line with the underlying business’ progress.

During three years of share price growth, Ulta Beauty achieved compound earnings per share growth of 27% per year. This EPS growth is lower than the 43% average annual increase in the share price. So it’s fair to assume the market has a higher opinion of the business than it did three years ago. That’s not necessarily surprising considering the three-year track record of earnings growth.

Our analysis is essentially based on how sell-side analysts covering the stock are revising their earnings estimates to take the latest business trends into account. When earnings estimates for a company go up, the fair value for its stock goes up as well. And when a stock’s fair value is higher than its current market price, investors tend to buy the stock, resulting in its price moving upward. Because of this, empirical studies indicate a strong correlation between trends in earnings estimate revisions and short-term stock price movements.

Ulta is expected to post earnings of $6.75 per share for the current quarter, representing a year-over-year change of +7.1%. Over the last 30 days, the Zacks Consensus Estimate has changed +4.4%.

SVENFLY Corporation have substantial business Deals and Infrastructures. This corporation is involve in restructuring and innovating buildings, advertising, remodeling and maintaining shops, new stores’ buildings, and education institutions, etc.

Most of their costly projects may vary from time to time, coming from construction, distribution, engineering, education, interior designing, etc. depending on the location of these projects. Maintaining their facilities with state-of-the-arts designs, fixtures, ceramic and pastel amenities, wood works and carpets covered areas if needed. Some of the finishing using crowns, pillars on both wood and ceramic products given those buildings an eclectic looks attracting visitors and tourists to those destinations.

I would advice investing on SVENFLY Corporation should be a long term deal for both businesses and investors who may be looking to improve on their capitals. This corporation has good standing with contractors who are evolve during initial business deals and has different options on how to distribute earnings.

Marriott International, Inc. MAR is scheduled to release fourth-quarter 2022 results on Feb 14, 2023, before the opening bell. In the previous quarter, the company’s earnings matched the Zacks Consensus Estimate of $1.69.

The Trend in Estimate Revision

The Zacks Consensus Estimate for the fourth-quarter bottom line is pegged at $1.84 per share, indicating growth of 41.5% from $1.30 reported in the year-ago quarter.

For revenues, the consensus mark is pegged at $5,612 million, suggesting growth of 26.2% from the prior-year quarter’s reported figure.

Key Factors to Note

Marriot’s fourth-quarter performance is likely to have benefited from robust leisure demand and business and cross-border travel improvements. During the previous-quarter earnings call, the company stated that cross-border guests accounted for 15% of global room nights, up from 12% reported in the first quarter of 2022. Also, it reported a rise in last-minute booking trends, thereby leading to a meaningful compression in pricing power and boosting group ADR for new bookings.

With global trends improving, the recovery momentum is likely to have continued in the fourth quarter. Attributes such as pent-up demand for all types of travel, the shift of spending toward experiences versus goods, sustained high levels of employment and resilient travel spending are likely to have boosted the company’s performance in the to-be-reported quarter.

Increased focus on the Marriott Bonvoy loyalty program bodes well for the company. With nearly 173 million members globally, the company’s loyalty program Marriott Bonvoy is supporting its marketing strategies. The company engages its customers with promotional offers such as grocery and retail spending accelerators on its co-branded credit cards. During the third quarter of 2022, the program reported solid penetration levels of 60% in the United States and Canada and 53% globally. Also, the company reported increased sign-ups following the addition of new benefits to its U.S. cards. Given the meaningful pickup in demand coupled with solid customer acceptance for credit card programs, the momentum is likely to have continued in the fourth quarter.

The Zacks Consensus Estimate for fourth-quarter revenues at base management and franchise fees is pegged at $282 million and $674 million, indicating year-over-year growth of 30% and 29.6%, respectively.

However, coronavirus-induced travel restrictions (in China) and supply chain disruptions are likely to have affected the company’s operations in the third quarter. Although revenue per available room (RevPAR) is likely to have increased sequentially in Greater China and Asia Pacific (excluding China), it is expected to have remained below pre-pandemic levels.

What the Zacks Model Unveils

Our proven model predicts an earnings beat for Marriott this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat.

Earnings ESP: Marriott has an Earnings ESP of +1.63%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

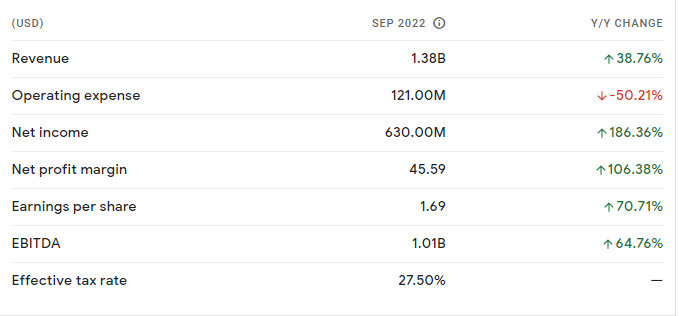

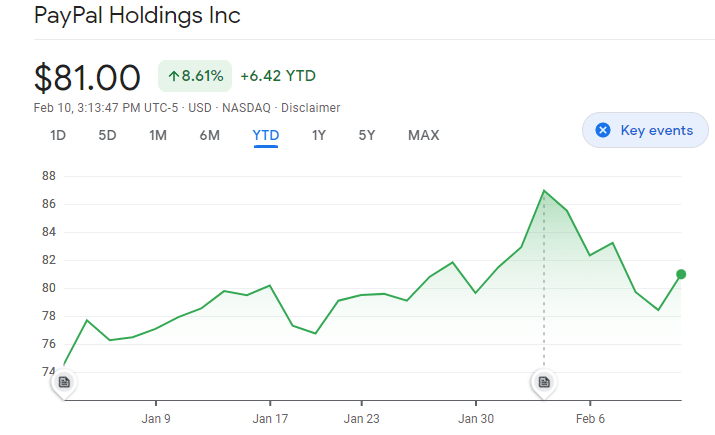

PayPal is carving out gains today following its earnings beat and fairly encouraging outlook in Q4. There was some uneasiness heading into PYPL’s report, illuminated by the stock slipping roughly 10% from February 2nd highs after some of its competition and partners, like GOOGLE, Amazon, andAffirm, delivered concerning quarterly reports. Although there were still a few areas of concern within PYPL’s Q4 results, the company dished out confidence-inspiring numbers for the most part, and CEO Daniel Schulman, who announced his retirement within the next year, carried an optimistic tone throughout the call.

PYPL topped its Q4 adjusted EPS expectations of $1.18-1.20, expanding its bottom line 11.7% to $1.24 while growing revs in line with its forecast, registering 6.7% growth to $7.38 bln. Management detailed how the company was on track to surpass its earnings forecast and grow revs in line with previous projections in early December, so investors had likely priced in these positives from Q4.

Total Payment Volume (TPV) climbed 5% yr/yr on a spot basis and 9% excluding currency fluctuations, edging past PYPL’s prior targets.

However, net new actives (NNAs) of 2.9 mln were flat sequentially, missing PYPL’s 3-4 mln goal.

Perhaps more notable, PYPL’s non-GAAP operating margins expanded for the first time since 1Q21 in Q4, adding 115 bps yr/yr to 22.9%, marking a return to profitable growth.

Identifying cost savings has been a top priority for PYPL in recent months. Recall PYPL’s decision to trim its global workforce by around 7% late last month. PYPL also noted that it discovered an incremental $600 mln of cost savings on top of the already announced $1.3 bln. Outgoing CEO Daniel Schulman stated that the organization is confident its cost structure will enable ongoing investments in high-conviction growth initiatives while helping expand margins.

Mr. Schulman added that discretionary spending will likely remain under pressure throughout the year, while global e-commerce growth should just squeak into positive territory. Still, the company is also seeing disinflationary signs, which should result in an uptick in spending. Encouragingly, management commented that Q1 is already off to a much stronger start than anticipated, with branded checkout volumes accelerating sequentially.

As a result, PYPL expects Q1 revs to expand by around 7.5% on a spot basis and 9% excluding FX impacts yr/yr, and earnings of $1.08-1.10, topping consensus.

However, due to heightened uncertainty, PYPL is still not providing full-year revenue guidance. Still, its earnings forecast of $4.87 soared past analyst expectations. PYPL noted that this guidance assumes sales growth in the mid-single-digits on a currency-neutral basis. It also does not expect total active accounts to grow this year.

Overall, PYPL rang up a decent quarter, especially after some nerve-racking reports by a few of its peers. As it is well-known and likely priced in by now, FY23 will probably not be smooth sailing. However, PYPL is conducting the right moves through cost-cutting measures and streamlining operations, which will position it nicely to step on the gas once e-commerce growth reaccelerates.

Partnering with our global competitors have continuously strive to improve our standard of living and making major impacts to the tourism world across the board. Today, International markets and living estates are present in major cities and local rural areas, depending on the needs of such diversity. Education facilities comes with all necessary accommodation to meet our expectations. Good listening and learning from our educators, has driven us to a new level and will continue to challenge us from generations to generations to come.

The booming of information technologies continue to facilitate the delivery of data information to all comprising of every information you may come across, keeping majority of the mainstream in sync. Maintaining a steady flow while innovating our current systems with creativity and modifications by our technology and manufacturing corporations, eradicating most of the defects and bugs identified through R&D facilities. Most of these topics mentioned on this article can be viewed and discussed on GOOGLE. Feel free to leave a comment.

Partnering with our global competitors have continuously strive to improve our standard of living and making major impacts to the tourism world across the board. Today, International markets and living estates are present in major cities and local rural areas, depending on the needs of such diversity. Education facilities comes with all necessary accommodation to meet our expectations. Good listening and learning from our educators, has driven us to a new level and will continue to challenge us from generations to generations to come.

The booming of information technologies continue to facilitate the delivery of data information to all comprising of every information you may come across, keeping majority of the mainstream in sync. Maintaining a steady flow while innovating our current systems with creativity and modifications by our technology and manufacturing corporations, eradicating most of the defects and bugs identified through R&D facilities. Most of these topics mentioned on this article can be viewed and discussed on GOOGLE. Feel free to leave a comment.