Some of Wall Street’s major stock indexes remain below their all-time highs, which means bargains can still be found.

Most online brokerages have done away with commission fees and minimum-deposit requirements, making it easier than ever for retail investors to put their money to work.

Three time-tested companies possess the necessary growth catalysts to make patient investors notably richer.

You don’t need a mountain of cash to build wealth on Wall Street.

Investing on Wall Street can sometimes be a roller coaster of emotions. The COVID-19 crash in February-March 2020 was the quickest bear market decline in history. Meanwhile, the rallies growth-stock investors have enjoyed in 2021 and 2023 have been jaw-dropping.

Despite these notable gains, some of Wall Street’s most followed indexes (e.g., the Nasdaq Composite) remain below their all-time closing highs. Put another way, high-quality stocks can still be purchased at a discount if you’re willing to put in the work and look for bargains.

What’s particularly noteworthy about putting your money to work on Wall Street is that prior barriers to investment have been all but torn down. Most online brokerages have completely done away with minimum-deposit requirements and commission fees for common stock trades executed on major U.S. exchanges. In other words, any amount of money — even $500 — can be the ideal amount to put to work.

If you have $500 that’s ready to invest, and this isn’t cash that’ll be needed to pay bills or cover an emergency, the following three stocks stand out as no-brainer buys right now.

Visa

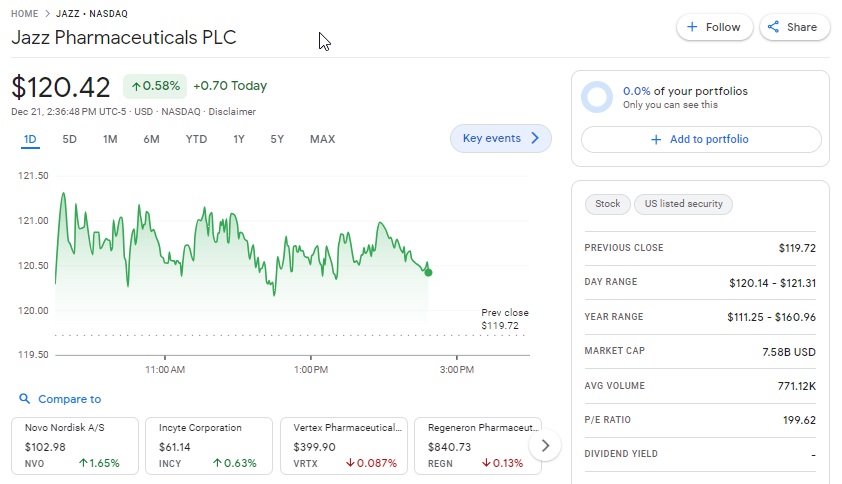

The first genius stock you can confidently add to your portfolio with $500 is world-leading payment processor Visa(V). Even though Visa shares are near an all-time high, the company sports a laundry list of competitive advantages that should continue to lift its valuation for years, if not decades, to come.

The interesting thing about Visa is that its biggest headwind is also its greatest opportunity. Like most financial stocks, Visa is cyclical. This is to say that its operating performance tends to ebb and flow with the health of the U.S. and global economy. If a recession takes place, consumer and enterprise spending would be expected to decline, leading to weaker fee collection for Visa.

However, the “ebbs” don’t last nearly as long as the “flows.” Only three of the 12 U.S. recessions since World War II have lasted at least one year. By comparison, most periods of expansion last multiple years, with two expansions lasting a full decade. Visa is perfectly positioned to take advantage of these extended periods of growth.

To add to the above point, Visa’s growth runway during these long-winded expansions is enormous. As of 2021, it held a nearly 53% share of credit card network-purchase volume in the United States. Meanwhile, faster-growing emerging-market regions, including the Middle East, Africa, and Southeastern Asia, remain largely underbanked and therefore ripe for disruption by financial-services providers like Visa.

Something else that’s been critical to Visa’s long-term success is its avoidance of lending. Visa is a well-known and trusted brand, and it would likely succeed as a lender. But doing so would also expose the company to credit delinquencies and loan losses during inevitable economic slowdowns. Completely avoiding the lending arena means not having to set aside capital for potential losses. It’s one of the key reasons Visa bounces back from recessions so quickly.

Lastly, Visa is a cash cow with a profit margin north of 50%. Although its forward price-to-earnings (P/E) ratio of 23 is higher than the benchmark S&P 500, Visa’s expected annualized earnings-growth rate of 14% over the next five years makes its stock a bargain.

Jazz Pharmaceuticals

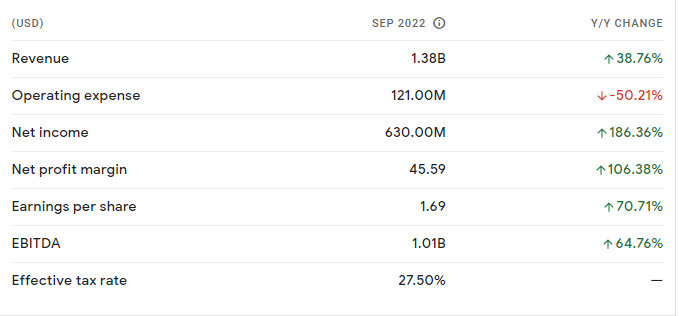

A second no-brainer stock with an exceptionally favorable risk-versus-reward profile for patient investors is specialty healthcare companyJazz Pharmaceuticals(JAZZ).

The enemy of pretty much every drug developer is time. Novel therapies have finite periods of sales exclusivity. Once those periods of exclusivity end, it’s not uncommon for generic drugs and/or biosimilar competition to enter the space and either siphon away sales or reduce the average selling price for a product. Jazz generates about half of its revenue from its oxybate franchise (Xywav and Xyrem), which help patients with various sleep disorders. A high concentration of sales in one franchise/area of focus can be worrisome.

However, Jazz Pharmaceuticals has its bases covered. The company developed a next-generation version of its narcolepsy blockbuster Xyrem. This new version, known as Xywav, contains 92% less sodium than its predecessor. Not only does this make Jazz’s drug safer to take for patients with higher cardiovascular risk factors, but it’ll help preserve the company’s cash flow and sales exclusivity for many years to come.

Jazz’s oncology portfolio is also gaining momentum. Cancer-drug sales look to be on track to reach $1 billion in 2023, with acute lymphoblastic leukemia therapy Rylaze doing a lot of the heavy lifting with sales up 46% year to date to $292.5 million.

Cannabidiol-based drug Epidiolex is holding its own as well. Since Jazz acquired GW Pharmaceuticals in May 2021 to get its hands on Epidiolex, sales have continued to grow. Additional worldwide approvals, along with label-expansion opportunities, have the ability to eventually push Epidiolex’s annual sales past $1 billion.

Don’t overlook Jazz’s pipeline, either. The company anticipates as many as five late-stage trial readouts before the end of 2024, with many of these advanced studies focused on experimental cancer drugs.

The third no-brainer stock to buy with $500 right now, conglomerate Berkshire Hathaway(BRK.A) (BRK.B), may not be a household name, but its billionaire CEO, Warren Buffett, certainly is. Take note, I’m specifically talking about Berkshire’s Class B shares (BRK.B), since a single Class A share will set an investor back more than $544,000!

Since the Oracle of Omaha became CEO in 1965, he’s overseen a 19.8% annualized return in his company’s Class A shares (BRK.A). The Class B shares weren’t issued until 1996, which is why I’m referring to returns of the Class A shares in this instance. Even if Berkshire fails to return close to 20% on an annualized basis moving forward, Buffett and his team have clearly demonstrated their ability to outpace the broader market over long periods.

One of the factors that makes Berkshire Hathaway such a special investment, other than Warren Buffett, is its focus on cyclical businesses.

Buffett and the late Charlie Munger, who served as Berkshire’s vice chairman for 45 years, realized a long time ago that betting on the U.S. economy to grow over time is a smart idea. Instead of trying to guess when recessions would occur, Buffett and Munger packed Berkshire’s investment portfolio and owned assets with time-tested, profitable, cyclical businesses. Thanks to extended periods of economic expansion, these long-term holdings have delivered big gains for Berkshire and its shareholders.

Another unsung hero for Berkshire Hathaway is the myriad of dividend stocks that sit in its investment portfolio. Over the course of the next year, Buffett and his investing aides will oversee the collection of around $6 billion in dividend income. On top of being recurringly profitable, dividend stocks have historically run circles around publicly traded companies that don’t offer a payout.

Furthermore, the culture that Charlie Munger instilled at Berkshire Hathaway is going to live on for decades to come. While every investor would love to see Warren Buffett live to be 120, the truth is that he and Munger built Berkshire Hathaway to succeed long after they’re gone. If the American economy is growing over time, there’s a good chance Berkshire’s wholly owned subsidiaries, which include insurer GEICO and railroad BNSF, as well as the company’s $374 billion investment portfolio, are going to benefit.

Should you invest $1,000 in Visa right now?

Before you buy stock in Visa, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Visa wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $294,765!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has nearly quadrupled the return of S&P 500 since 2002*.

With a net worth of $250 billion, Elon Musk is officially the wealthiest person on earth.

And with an IQ of 155, he’s also one of the smartest.

However, by openly advocating for a type of energy that the U.S. military says could have a “significant impact on the army, our allies, the international community, the commercial power industry, and the nation…”

And even though you may not know it, or even care…

The coming war on Elon Musk is going to have a direct impact on you, your family, and your financial investments in the years to come.

In this new exposé, you’ll learn what it is that Elon has discovered, and how you can profit from it in the months and years to come. Check it out here…

It was the best half-year for billionaires since the back half of 2020, when the economy rebounded from a Covid-induced slump.

The gains coincided with a broad stock market rally, as investors brushed off the effects of central bank interest rate hikes, the ongoing war in Ukraine and a crisis in regional banks. The S&P 500 rose 16% and the Nasdaq 100 surged 39% for its best-ever first half as investor mania over artificial intelligence boosted tech stocks. Here’s a link to this article.

SVENFLY Corporation is widely known in most industrial cities in the world. This corporation produces articles, items, apparel, and invest heavily on transportation, manufacturing, distribution and infrastructures expanding developed countries and cities around the world. SVEN Corporation changed it’s name to SVENFLY Corporation in September 2020.

Investment and Productivity of similar corporations like this may not be apparent to the public. The advertising markets is playing a huge role by discussing and attracting investors to purchase this corporation’s products.

The number SEVEN is frequently used on most of it’s properties. An ancient myth has always viewed this number to be a lucky number, and it has always been so and will continue in generations and generations to come.

This corporation was introduce in the market during the third quarter of 1998 and have had it’s ups and downs just like any stock on the market. The key founder(s) have being disappointed with it’s performance but with company restructure and reorganization, they are looking forward to breakthroughs, making reasonable decisions to outperform some of their competitors. Portfolio manager(s) / analyst(s) have also play a good part by reporting how well SVENFLY Corporation is performing around the world.

New attractions and interest into major construction endeavors has driven the expansion and remodel of the world’s major cities, meeting the needs and expectations of group activities to be able to take place wherever scheduled. The planning and redistribution of funds into projects such as these across the board comes with its challenges, keeping the crews alert throughout the lifecycle of such major projects. Management, entertainment, amenities, and supplies play a key role in running these businesses within most of our magnificent locations, moving employees from one location to another, keeping a steady flow and expectations to our guests.

Our utilities facilities and subsidiary corporations are working continuously around the clock, making sure our main necessities and supplies are met from fuel gasoline, hydrate fuel, expansion and

maintenance of roads, water supplies and food delivery trucking coast to coast. Our power generation systems and auxiliaries wind mills power supplies can seen and spotted along our highways which

cannot be taken for granted. We are blessed to have both rural and urban amenities to balance our ecosystems, keeping us in check and competitive with our global competitors.

Partnering with our global competitors have continuously strive to improve our standard of living and making major impacts to the tourism world across the board. Today, International markets and living estates are present in major cities and local rural areas, depending on the needs of such diversity. Education facilities comes with all necessary accommodation to meet our expectations. Good listening and learning from our educators, has driven us to a new level and will continue to challenge us from generations to generations to come.

The booming of information technologies continue to facilitate the delivery of data information to all comprising of every information you may come across, keeping majority of the mainstream in sync. Maintaining a steady flow while innovating our current systems with creativity and modifications by our technology and manufacturing corporations, eradicating most of the defects and bugs identified through R&D facilities. Most of these topics mentioned on this article can be viewed and discussed on GOOGLE. Feel free to leave a comment.

Involving business when developing suburbs and inner cities, it is necessary and helpful to bring different construction business together to work and partner as teams. These construction contractors / business intend becomes affiliated to related defined projects as such while development becomes identify and progresses throughout different locations. The bonding formed during such constructions go a long way and should be nurtured by maintaining the same group of construction corporations while introducing new once into the market.

Capitalism on performance and profitability has driven business in to a new height, keeping their goals in positive momentum while addressing remodeling and maintaining their structures. The infrastructure units necessary for such developments may be put in place by one or many construction business depending on the magnitude and location of the projects.

Feasibility studies of similar projects are mostly used in deriving the current expense of newly defined projects to come up with a ballpark estimate before involving regular investors into the business deal. Its’ always nice to have projected deals lined up although the constant continuity set forth for these corporations to advertise their projects are necessary to maintain their customers and clients, to strive in meeting the companies’ bottom line giving investors a reason to invest in their markets and corporations.

SVEN Corporation is a typical corporation doing business in many sectors to meet up with the demand of both population and location driven business both locally and globally depending on the demands. I will advice investors to depend and invest on corporations like this. Good timing to hold and buy.

One simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

The most you can lose on any stock (assuming you don’t use leverage) is 100% of your money. But in contrast you can make much more than 100% if the company does well. For instance the Ulta Beauty, Inc. share price is 191% higher than it was three years ago. Most would be happy with that. It’s also good to see the share price up 13% over the last quarter. But this could be related to the strong market, which is up 6.2% in the last three months.

So let’s investigate and see if the longer term performance of the company has been in line with the underlying business’ progress.

During three years of share price growth, Ulta Beauty achieved compound earnings per share growth of 27% per year. This EPS growth is lower than the 43% average annual increase in the share price. So it’s fair to assume the market has a higher opinion of the business than it did three years ago. That’s not necessarily surprising considering the three-year track record of earnings growth.

Our analysis is essentially based on how sell-side analysts covering the stock are revising their earnings estimates to take the latest business trends into account. When earnings estimates for a company go up, the fair value for its stock goes up as well. And when a stock’s fair value is higher than its current market price, investors tend to buy the stock, resulting in its price moving upward. Because of this, empirical studies indicate a strong correlation between trends in earnings estimate revisions and short-term stock price movements.

Ulta is expected to post earnings of $6.75 per share for the current quarter, representing a year-over-year change of +7.1%. Over the last 30 days, the Zacks Consensus Estimate has changed +4.4%.

SVENFLY Corporation have substantial business Deals and Infrastructures. This corporation is involve in restructuring and innovating buildings, advertising, remodeling and maintaining shops, new stores’ buildings, and education institutions, etc.

Most of their costly projects may vary from time to time, coming from construction, distribution, engineering, education, interior designing, etc. depending on the location of these projects. Maintaining their facilities with state-of-the-arts designs, fixtures, ceramic and pastel amenities, wood works and carpets covered areas if needed. Some of the finishing using crowns, pillars on both wood and ceramic products given those buildings an eclectic looks attracting visitors and tourists to those destinations.

I would advice investing on SVENFLY Corporation should be a long term deal for both businesses and investors who may be looking to improve on their capitals. This corporation has good standing with contractors who are evolve during initial business deals and has different options on how to distribute earnings.

Marriott International, Inc. MAR is scheduled to release fourth-quarter 2022 results on Feb 14, 2023, before the opening bell. In the previous quarter, the company’s earnings matched the Zacks Consensus Estimate of $1.69.

The Trend in Estimate Revision

The Zacks Consensus Estimate for the fourth-quarter bottom line is pegged at $1.84 per share, indicating growth of 41.5% from $1.30 reported in the year-ago quarter.

For revenues, the consensus mark is pegged at $5,612 million, suggesting growth of 26.2% from the prior-year quarter’s reported figure.

Key Factors to Note

Marriot’s fourth-quarter performance is likely to have benefited from robust leisure demand and business and cross-border travel improvements. During the previous-quarter earnings call, the company stated that cross-border guests accounted for 15% of global room nights, up from 12% reported in the first quarter of 2022. Also, it reported a rise in last-minute booking trends, thereby leading to a meaningful compression in pricing power and boosting group ADR for new bookings.

With global trends improving, the recovery momentum is likely to have continued in the fourth quarter. Attributes such as pent-up demand for all types of travel, the shift of spending toward experiences versus goods, sustained high levels of employment and resilient travel spending are likely to have boosted the company’s performance in the to-be-reported quarter.

Increased focus on the Marriott Bonvoy loyalty program bodes well for the company. With nearly 173 million members globally, the company’s loyalty program Marriott Bonvoy is supporting its marketing strategies. The company engages its customers with promotional offers such as grocery and retail spending accelerators on its co-branded credit cards. During the third quarter of 2022, the program reported solid penetration levels of 60% in the United States and Canada and 53% globally. Also, the company reported increased sign-ups following the addition of new benefits to its U.S. cards. Given the meaningful pickup in demand coupled with solid customer acceptance for credit card programs, the momentum is likely to have continued in the fourth quarter.

The Zacks Consensus Estimate for fourth-quarter revenues at base management and franchise fees is pegged at $282 million and $674 million, indicating year-over-year growth of 30% and 29.6%, respectively.

However, coronavirus-induced travel restrictions (in China) and supply chain disruptions are likely to have affected the company’s operations in the third quarter. Although revenue per available room (RevPAR) is likely to have increased sequentially in Greater China and Asia Pacific (excluding China), it is expected to have remained below pre-pandemic levels.

What the Zacks Model Unveils

Our proven model predicts an earnings beat for Marriott this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat.

Earnings ESP: Marriott has an Earnings ESP of +1.63%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

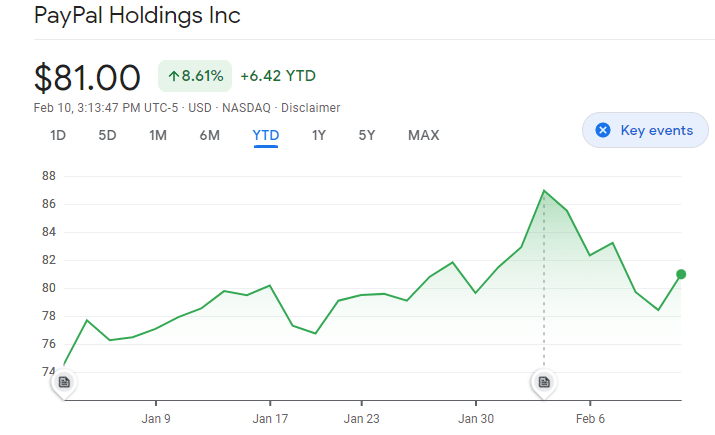

PayPal is carving out gains today following its earnings beat and fairly encouraging outlook in Q4. There was some uneasiness heading into PYPL’s report, illuminated by the stock slipping roughly 10% from February 2nd highs after some of its competition and partners, like GOOGLE, Amazon, andAffirm, delivered concerning quarterly reports. Although there were still a few areas of concern within PYPL’s Q4 results, the company dished out confidence-inspiring numbers for the most part, and CEO Daniel Schulman, who announced his retirement within the next year, carried an optimistic tone throughout the call.

PYPL topped its Q4 adjusted EPS expectations of $1.18-1.20, expanding its bottom line 11.7% to $1.24 while growing revs in line with its forecast, registering 6.7% growth to $7.38 bln. Management detailed how the company was on track to surpass its earnings forecast and grow revs in line with previous projections in early December, so investors had likely priced in these positives from Q4.

Total Payment Volume (TPV) climbed 5% yr/yr on a spot basis and 9% excluding currency fluctuations, edging past PYPL’s prior targets.

However, net new actives (NNAs) of 2.9 mln were flat sequentially, missing PYPL’s 3-4 mln goal.

Perhaps more notable, PYPL’s non-GAAP operating margins expanded for the first time since 1Q21 in Q4, adding 115 bps yr/yr to 22.9%, marking a return to profitable growth.

Identifying cost savings has been a top priority for PYPL in recent months. Recall PYPL’s decision to trim its global workforce by around 7% late last month. PYPL also noted that it discovered an incremental $600 mln of cost savings on top of the already announced $1.3 bln. Outgoing CEO Daniel Schulman stated that the organization is confident its cost structure will enable ongoing investments in high-conviction growth initiatives while helping expand margins.

Mr. Schulman added that discretionary spending will likely remain under pressure throughout the year, while global e-commerce growth should just squeak into positive territory. Still, the company is also seeing disinflationary signs, which should result in an uptick in spending. Encouragingly, management commented that Q1 is already off to a much stronger start than anticipated, with branded checkout volumes accelerating sequentially.

As a result, PYPL expects Q1 revs to expand by around 7.5% on a spot basis and 9% excluding FX impacts yr/yr, and earnings of $1.08-1.10, topping consensus.

However, due to heightened uncertainty, PYPL is still not providing full-year revenue guidance. Still, its earnings forecast of $4.87 soared past analyst expectations. PYPL noted that this guidance assumes sales growth in the mid-single-digits on a currency-neutral basis. It also does not expect total active accounts to grow this year.

Overall, PYPL rang up a decent quarter, especially after some nerve-racking reports by a few of its peers. As it is well-known and likely priced in by now, FY23 will probably not be smooth sailing. However, PYPL is conducting the right moves through cost-cutting measures and streamlining operations, which will position it nicely to step on the gas once e-commerce growth reaccelerates.

Kgoo Episode 59

Kgoo Episode 59