With a net worth of $250 billion, Elon Musk is officially the wealthiest person on earth.

And with an IQ of 155, he’s also one of the smartest.

However, by openly advocating for a type of energy that the U.S. military says could have a “significant impact on the army, our allies, the international community, the commercial power industry, and the nation…”

And even though you may not know it, or even care…

The coming war on Elon Musk is going to have a direct impact on you, your family, and your financial investments in the years to come.

In this new exposé, you’ll learn what it is that Elon has discovered, and how you can profit from it in the months and years to come. Check it out here…

It was the best half-year for billionaires since the back half of 2020, when the economy rebounded from a Covid-induced slump.

The gains coincided with a broad stock market rally, as investors brushed off the effects of central bank interest rate hikes, the ongoing war in Ukraine and a crisis in regional banks. The S&P 500 rose 16% and the Nasdaq 100 surged 39% for its best-ever first half as investor mania over artificial intelligence boosted tech stocks. Here’s a link to this article.

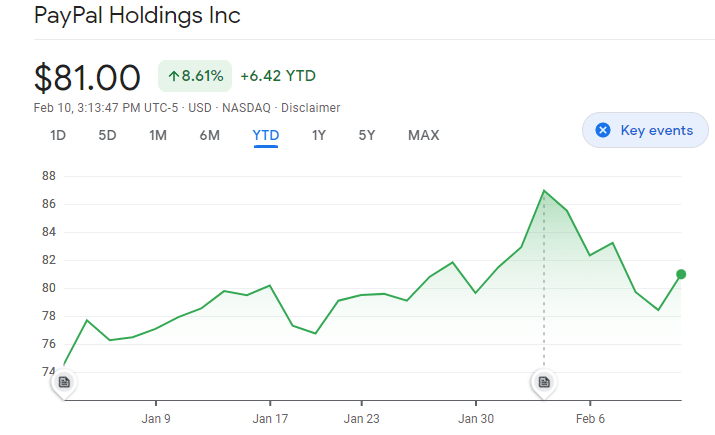

PayPal is carving out gains today following its earnings beat and fairly encouraging outlook in Q4. There was some uneasiness heading into PYPL’s report, illuminated by the stock slipping roughly 10% from February 2nd highs after some of its competition and partners, like GOOGLE, Amazon, andAffirm, delivered concerning quarterly reports. Although there were still a few areas of concern within PYPL’s Q4 results, the company dished out confidence-inspiring numbers for the most part, and CEO Daniel Schulman, who announced his retirement within the next year, carried an optimistic tone throughout the call.

PYPL topped its Q4 adjusted EPS expectations of $1.18-1.20, expanding its bottom line 11.7% to $1.24 while growing revs in line with its forecast, registering 6.7% growth to $7.38 bln. Management detailed how the company was on track to surpass its earnings forecast and grow revs in line with previous projections in early December, so investors had likely priced in these positives from Q4.

Total Payment Volume (TPV) climbed 5% yr/yr on a spot basis and 9% excluding currency fluctuations, edging past PYPL’s prior targets.

However, net new actives (NNAs) of 2.9 mln were flat sequentially, missing PYPL’s 3-4 mln goal.

Perhaps more notable, PYPL’s non-GAAP operating margins expanded for the first time since 1Q21 in Q4, adding 115 bps yr/yr to 22.9%, marking a return to profitable growth.

Identifying cost savings has been a top priority for PYPL in recent months. Recall PYPL’s decision to trim its global workforce by around 7% late last month. PYPL also noted that it discovered an incremental $600 mln of cost savings on top of the already announced $1.3 bln. Outgoing CEO Daniel Schulman stated that the organization is confident its cost structure will enable ongoing investments in high-conviction growth initiatives while helping expand margins.

Mr. Schulman added that discretionary spending will likely remain under pressure throughout the year, while global e-commerce growth should just squeak into positive territory. Still, the company is also seeing disinflationary signs, which should result in an uptick in spending. Encouragingly, management commented that Q1 is already off to a much stronger start than anticipated, with branded checkout volumes accelerating sequentially.

As a result, PYPL expects Q1 revs to expand by around 7.5% on a spot basis and 9% excluding FX impacts yr/yr, and earnings of $1.08-1.10, topping consensus.

However, due to heightened uncertainty, PYPL is still not providing full-year revenue guidance. Still, its earnings forecast of $4.87 soared past analyst expectations. PYPL noted that this guidance assumes sales growth in the mid-single-digits on a currency-neutral basis. It also does not expect total active accounts to grow this year.

Overall, PYPL rang up a decent quarter, especially after some nerve-racking reports by a few of its peers. As it is well-known and likely priced in by now, FY23 will probably not be smooth sailing. However, PYPL is conducting the right moves through cost-cutting measures and streamlining operations, which will position it nicely to step on the gas once e-commerce growth reaccelerates.